Why it’s better to be a Real Estate Agent than a Stockbroker in 2026

Published July 6th 2026

It’s been a long time since I made my start in finance in 2008. I was working on Eagle Street in Riparian Plaza in the back office of a prominent Brisbane stockbroking firm called Wilson HTM. Our team were responsible for settling the firm’s domestic trades. At the time, I didn’t fully appreciate that I was at the epicentre of the GFC here in Brisbane in 2008.

I was settling the trades where the investor had borrowed money to buy stocks. As stock prices started to fall, I was then transferring stocks to the margin lenders to avoid margin calls for clients. Up until then, the market was hot and the stockbrokers were kings. When I got the job, I thought this would be my path. The first rock in the road was a redundancy in September 2008 right as the GFC hit the world.

After that, margin lending was used far less often for retail investors and I was able to make a start in international settlements at Morgans Stockbroking. Here, our small team ensured the settlement of the firm’s trading activity in all stocks outside of Australia, including all currency conversions. It was here that I realised just how much of our client’s trading activity was focused primarily at home in Oz. We may hear all about the hot stocks in the US but most Aussie stockbrokers focus domestically.

I then moved to economics consulting at KPMG from 2011 - 2013 where I worked on some large projects and developed the skills to write this report as well as the confidence to move overseas. After a short break in Toronto, Canada, I became a financial advisor in 2014 at Investors Group and a buyers agent at Zoocasa in 2015. That experience in financial planning helped me better realise the benefit in purchasing tax effective assets like property that can also double as consumption spending for your principal primary residence (PPR).

In Australia, when you’re investing someone’s assets in stockbroking, it’s either in their super fund or it’s their extra cash. After watching property go through the roof in Toronto through to 2017, I witnessed what it was like for people to put all their spare money into property. After a short stint as a stockbroker back in Brisbane, I later became a listing agent at Pure Real Estate from 2020 - 2022 and Ray White Bulimba between 2022 - 2023. As you know, many regular Queenslanders are now putting all their cash into their primary residence.

I was there to see the fall of the global stock market in 2008, I bought stocks in 2009 and witnessed their rise here in Australia then I sold them and used the profits to move to Canada where I learned funds management and financial planning. I was there to witness the rise of the Canadian housing market as a buyer’s agent through to 2017. When I stepped back into property as a listing agent in Brisbane in 2020, I worked mainly with investors and sold most of my listings to young owner occupiers. I was there for the rise of the Aussie property market during the GFC and I was part of the industry when real estate agents became the new stockbrokers and Aussies became even more obsessed with property.

I trained with some of the best agents in Brisbane at the biggest Ray White Agency in Australia as part of the Ray White Collective with Haesley Cush, Matt Lancashire, Scotty Darwon & Brandon Wortley. I want to now look back over that whole 2008 - 2026 period to look at stocks VS property from a capital gains perspective here in Australia.

On the race to the global financial markets peak in 2008, many people borrowed money to buy stocks. Plenty of stocks then essentially halved at the end of 2008. By the time the market started hitting its stride in 2009, many were gun shy and unwilling to take out loans to buy stocks again. I was there to see all this, look at the target price of the firm’s stocks from the research department then do a quick check to see where the price was at its previous peak. I was a complete amateur but it became normal for me for stocks to double within a year then I would need to wait for the full 12 month period to sell them to ensure I received the 50% capital gains tax discount. If that were to happen again, investors would get taxed more on a sharp gain, even if they were young low income earners like I was at the time.

I don’t speak about finance much anymore but I’ve also had the benefit of regular chats with one of my first mentors, Marcel, one of the best minds in Brisbane when it comes to finance, economics and Government policy. Today, I’d like to run through a few of the underlying influences that have led to the Government making some changes to capital gains tax and negative gearing to increase revenue from capital, not just income tax. These changes significantly impact the two industries where I spent most of my career, property & finance. Unfortunately, the sentiment behind these policies is not new. Capital in the 21st Century by Thomas Piketty was published in 2014, along with the wealth tax recommendation, as below.

“What is the ideal schedule for a tax on capital, and how much would such a tax bring in? To be clear, I am speaking here of a permanent annual tax on capital at a rate that must therefore be fairly moderate. A tax collected only once a generation, such as an inheritance tax, can be assessed at a very high rate: a third, a half, or even two-thirds, as was the case for the largest estates in Britain and the United States from 1930 to 1980. The same is true of exceptional one-time taxes on capital levied in unusual circumstances, such as the tax levied on capital in France in 1945 at rates as high as 25 percent, indeed 100 percent for additions to capital during the Occupation (1940–1945). Clearly, such taxes cannot be applied for very long: if the government takes a quarter of the nation’s wealth every year, there will be nothing left to tax after a few years.

That is why the rates of an annual tax on capital must be much lower, on the order of a few percent. To some this may seem surprising, but it is actually quite a substantial tax, since it is levied every year on the total stock of capital. For example, the property tax rate is frequently just 0.5–1 percent of the value of real estate, or a tenth to a quarter of the rental value of the property (assuming an average rental return of 4 percent a year). The next point is important, and I want to insist on it: given the very high level of private wealth in Europe today, a progressive annual tax on wealth at modest rates could bring in significant revenue. Take, for example, a wealth tax of 0 percent on fortunes below 1 million euros, 1 percent between 1 and 5 million euros, and 2 percent above 5 million euros. If applied to all member states of the European Union, such a tax would affect about 2.5 percent of the population and bring in revenues equivalent to 2 percent of Europe’s GDP. The high return should come as no surprise: it is due simply to the fact that private wealth in Europe today is worth more than five years of GDP, and much of that wealth is concentrated in the upper centiles of the distribution.” Thomas Piketty - Capital in the 21st Century

The Netherlands has recently decided to implement a tax of 36% on unrealised stock, bond and crypto gains. Interestingly, property was left out of that deal. Australia has just started the process of reconsidering capital gains tax and withdrawing negative gearing from existing properties. As our country ages and taxation revenue from income wanes, I expect this may be just the beginning - I also hope I’m wrong. That still won’t change the fact that Aussies love property and it’s a whole lot easier to understand than investing in stocks and bonds.

Now that the scene has been set, let’s look at some data. I would usually do all the data analysis myself however all these images and graphs were created by ChatGPT. I’ll aim to keep the commentary to a minimum. My aim here is to talk through the basic trends rather than present perfect data that would take weeks to create. In saying that, you’ll likely also see analysis here from more angles than you may have seen elsewhere. This is all just to start a conversation and to paint the broader picture so you can walk through the details with your clients from a range of perspectives.

*ChatGPT may have been slightly inconsistent with the dataset at times, so apologies if you notice any errors. As I said above, the goal is discuss obvious trends rather than perfect data.

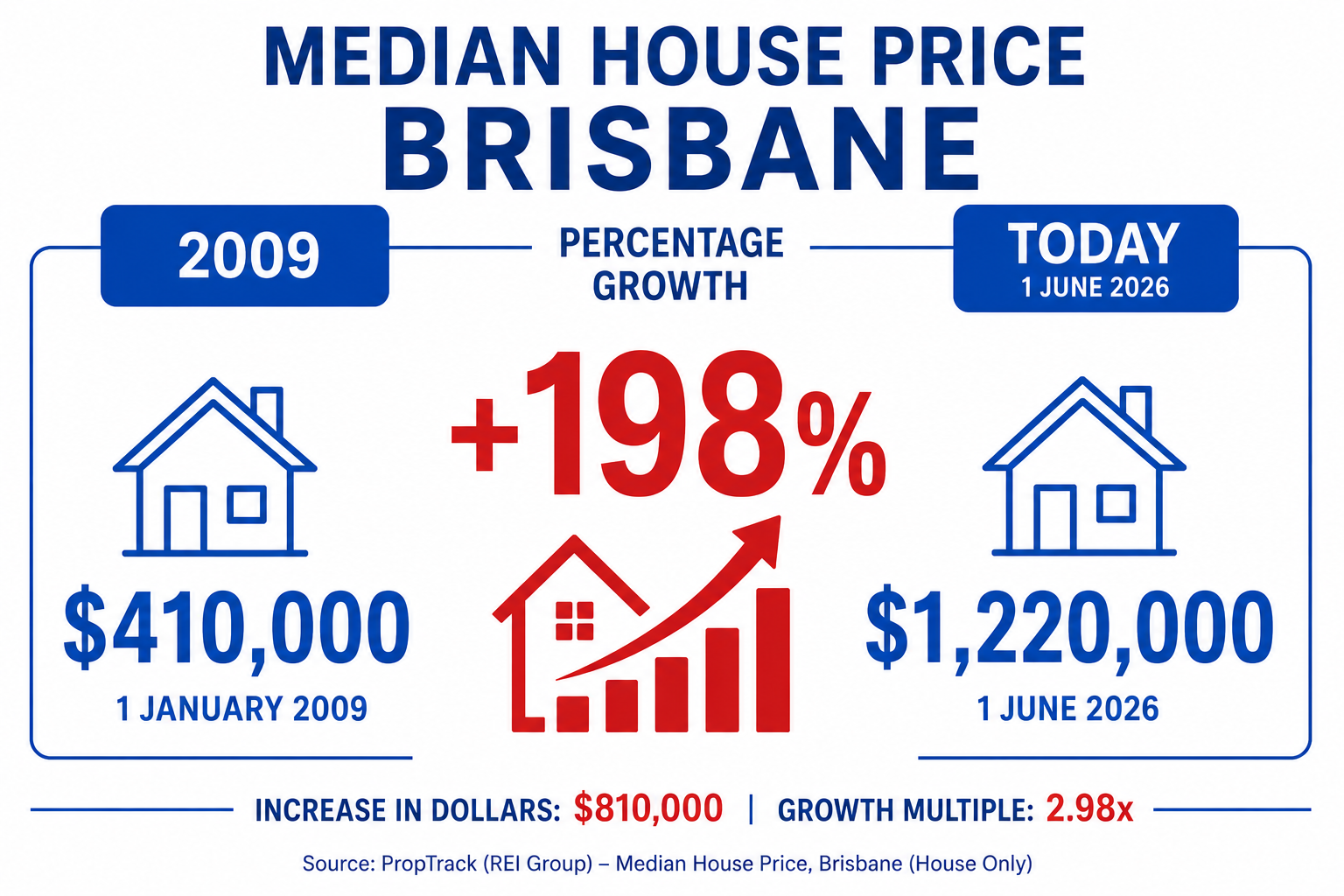

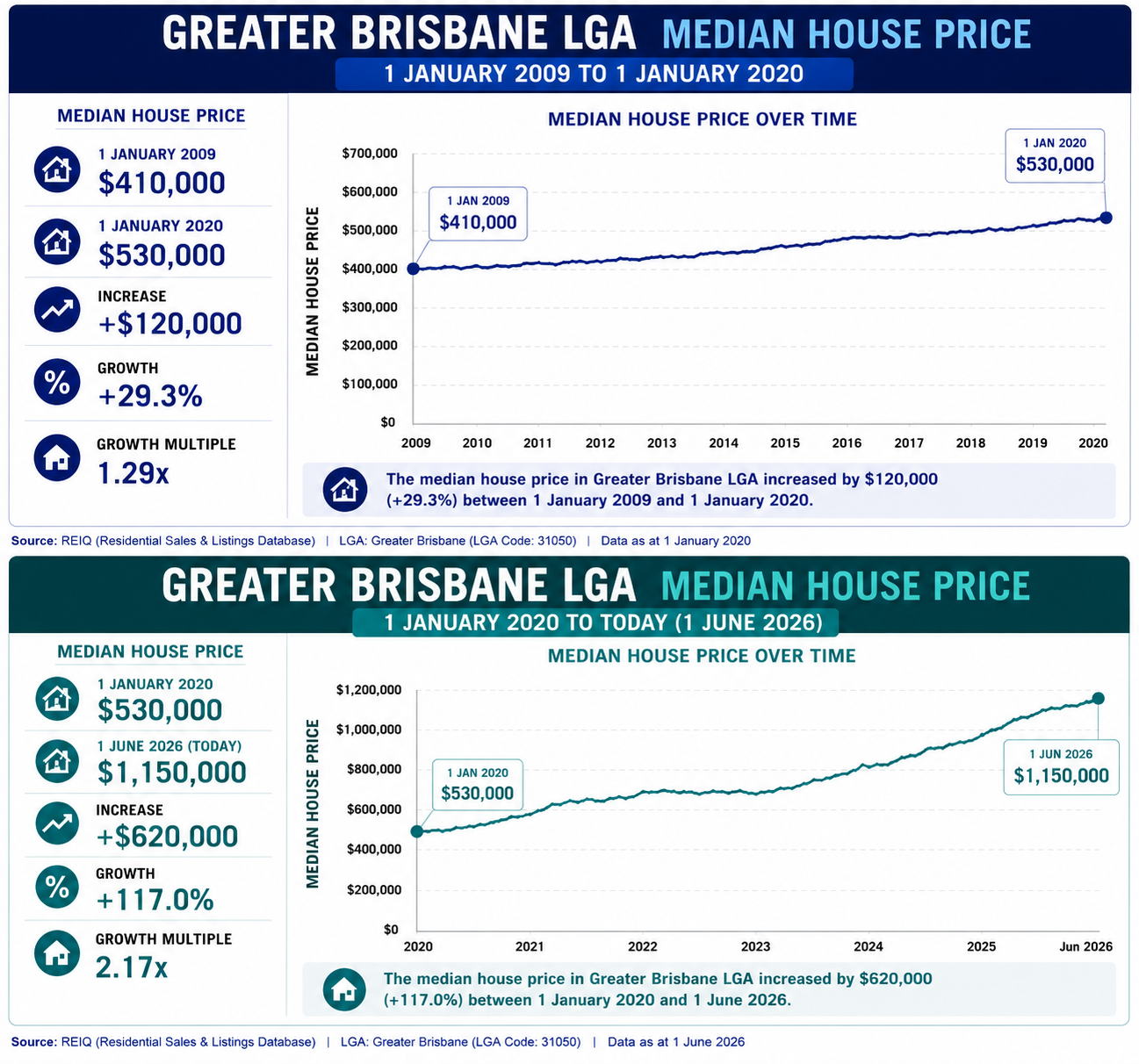

Property almost tripled in Brisbane between Jan 2009 - June 2026 while the ASX200 stock market index grew by 140%, with the majority of its gain between 2009 - 2020, as below.

As you can see above and below, the ideal trade would have been to hold shares until 2020 then switch into property to pick up the highest growth periods in each asset class.

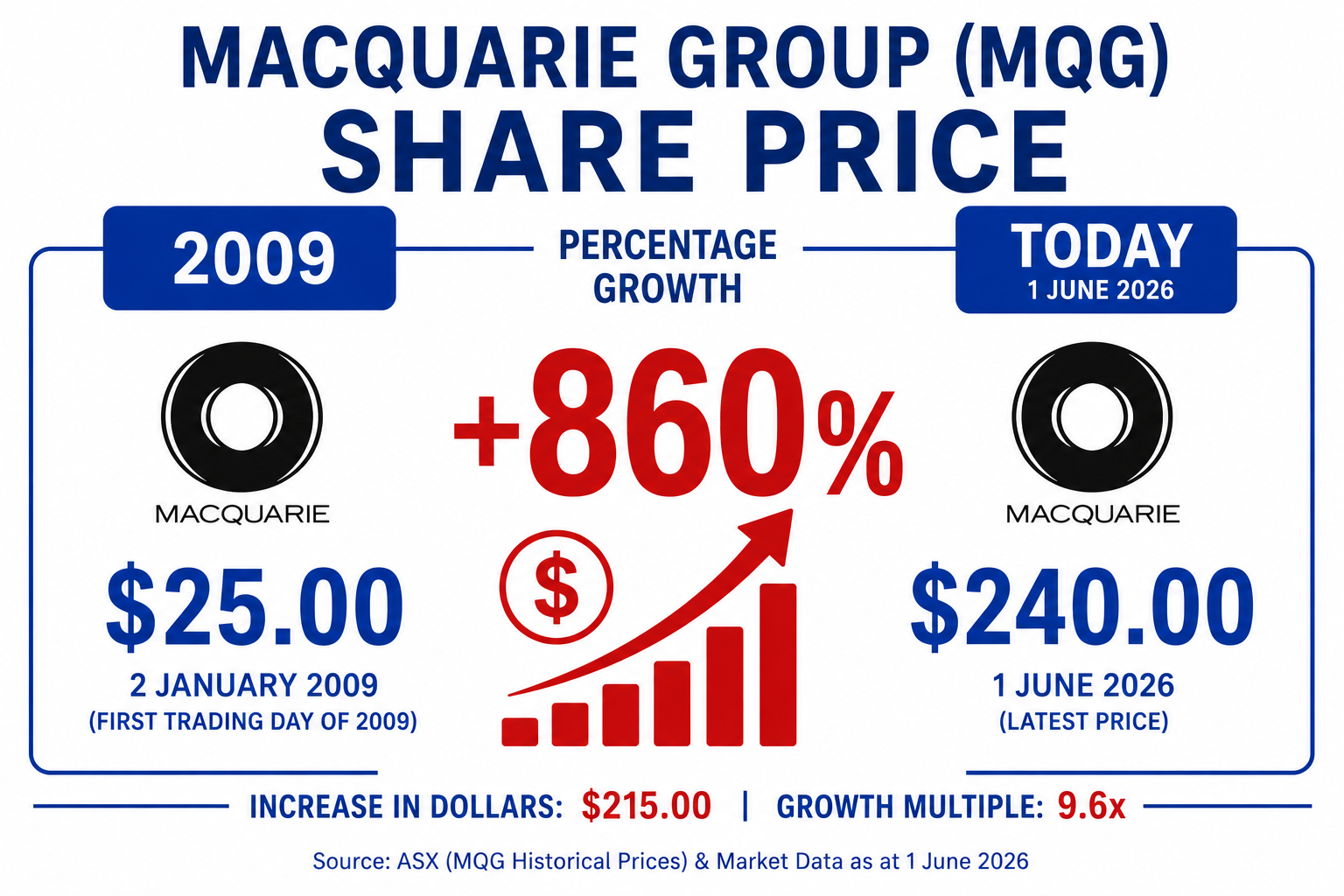

There were still significant gains available in some stocks, like Macquarie Group (MQG) which grew to almost 10 times its price in 2009 by 1 June 2026.

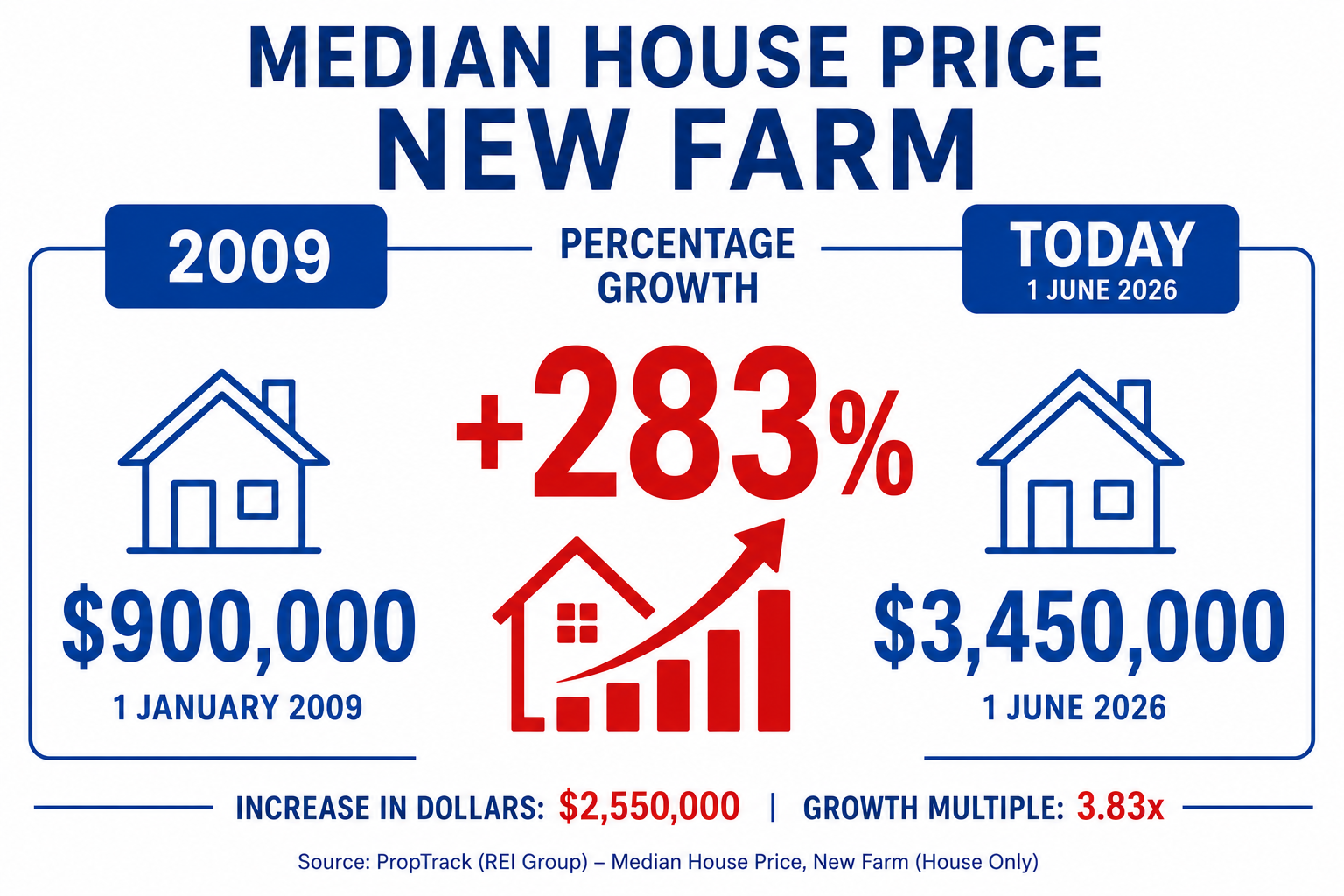

At the same time, some suburbs, like New Farm, outperformed wider Brisbane with a median price that is almost four times its 2009 price, post GFC.

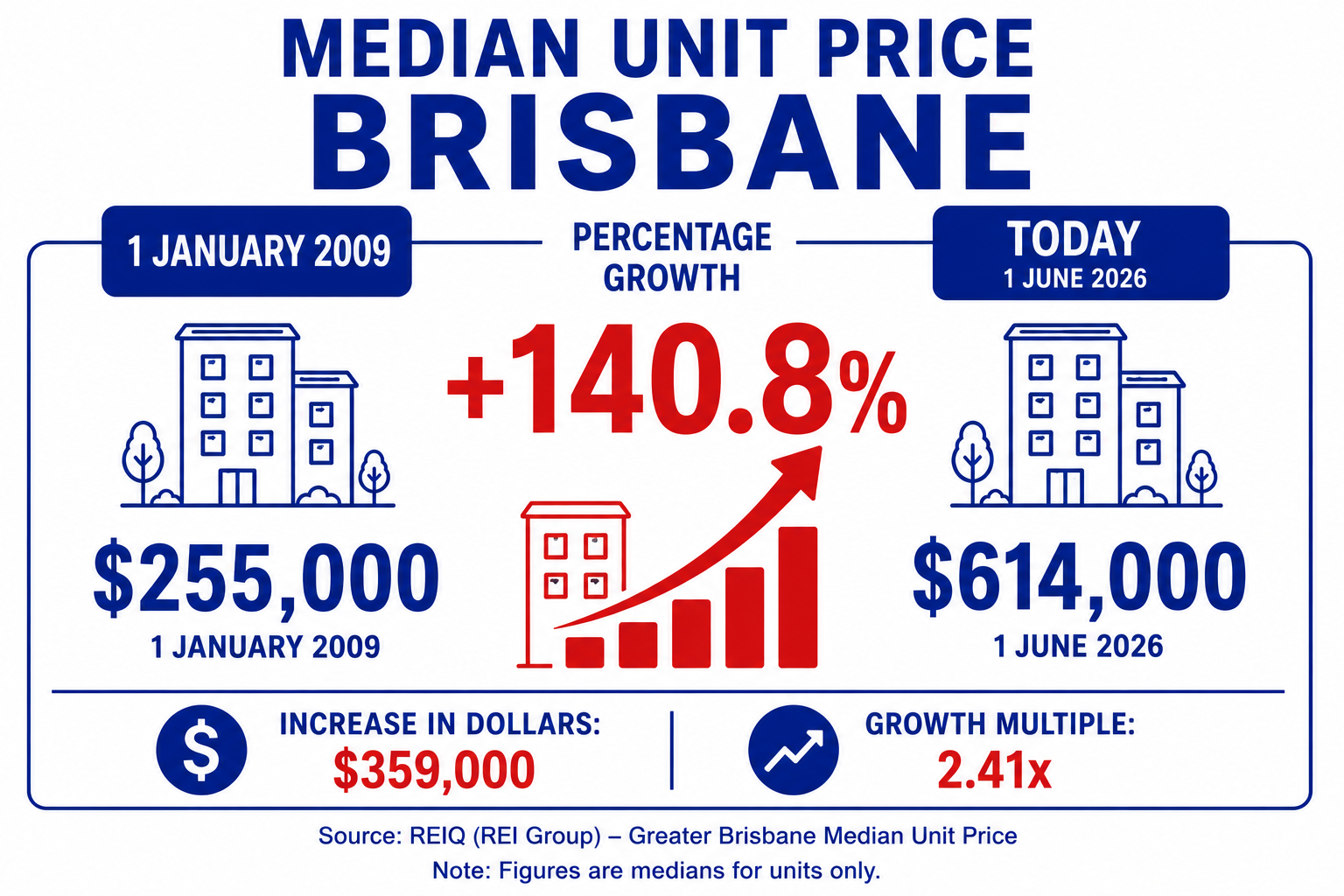

When I was selling off the rent roll between 2020 - 2022, I sold a lot of units and townhouses as this was often the period where they saw the first significant capital growth in over a decade. As can be seen below, owning a unit in Brisbane achieved similar growth (140%) as holding the ASX200 index between January 2009 to June 2026. The difference is that the unit is probably higher leveraged than the share portfolio which allows the holding to be much larger. As you know, there’s also significant income upside in the unit, not just capital growth. In saying that, this was also the first time in a long time where this investor stock actually achieved decent capital growth rather than just good yields.

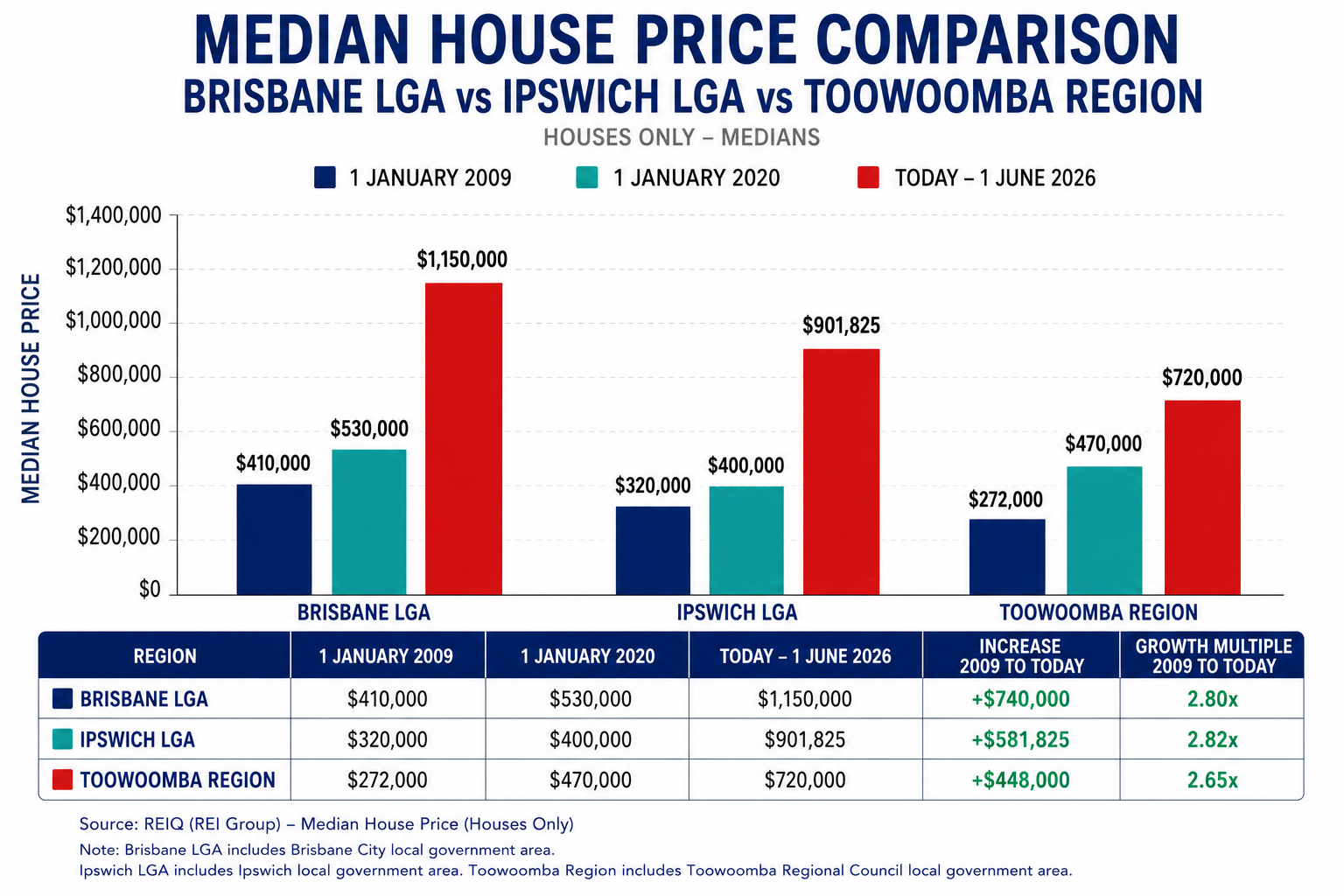

There was also significant growth for houses in regional areas like Ipswich & Toowoomba, as below.

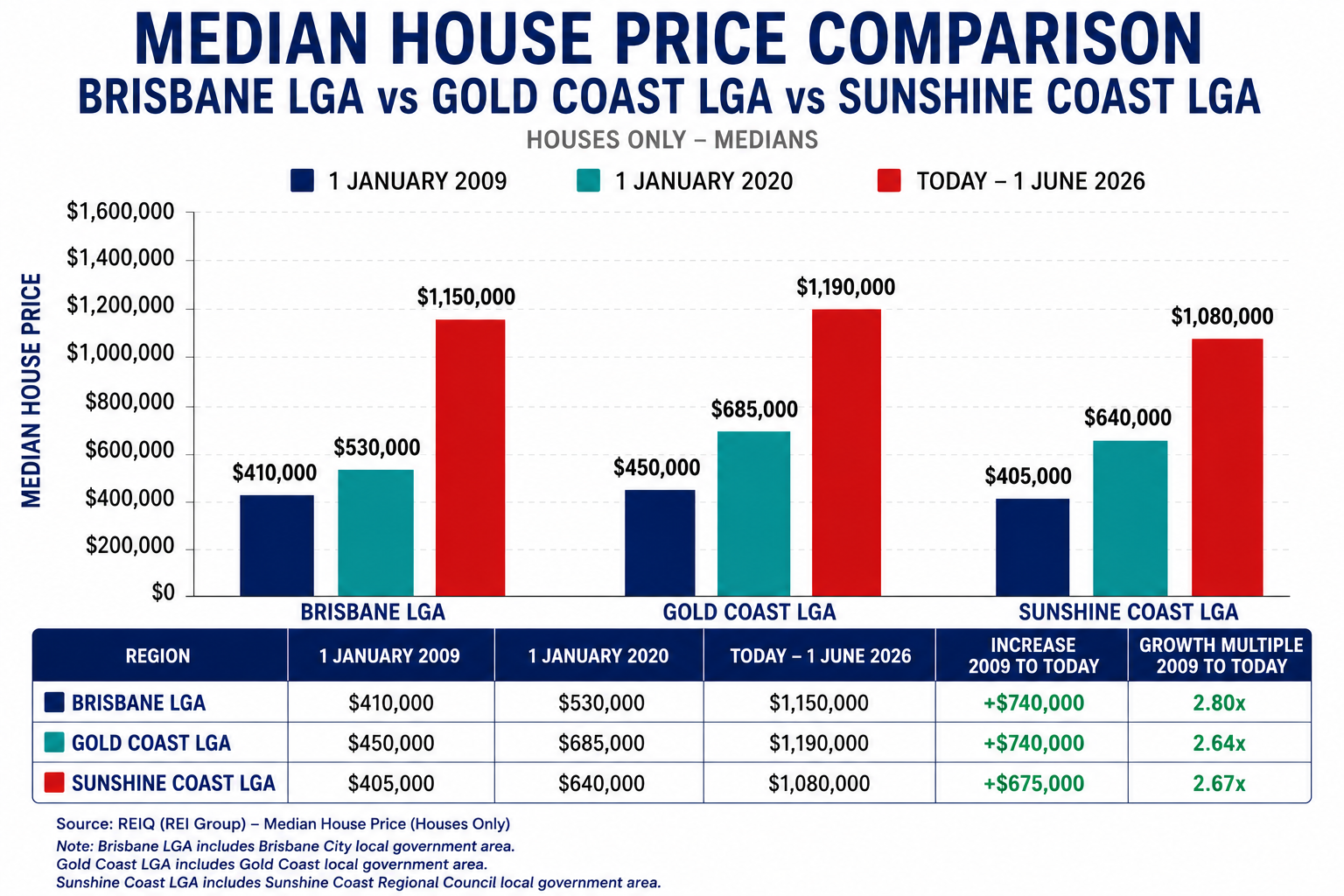

Growth was also very strong at the Gold Coast & Sunshine Coast.

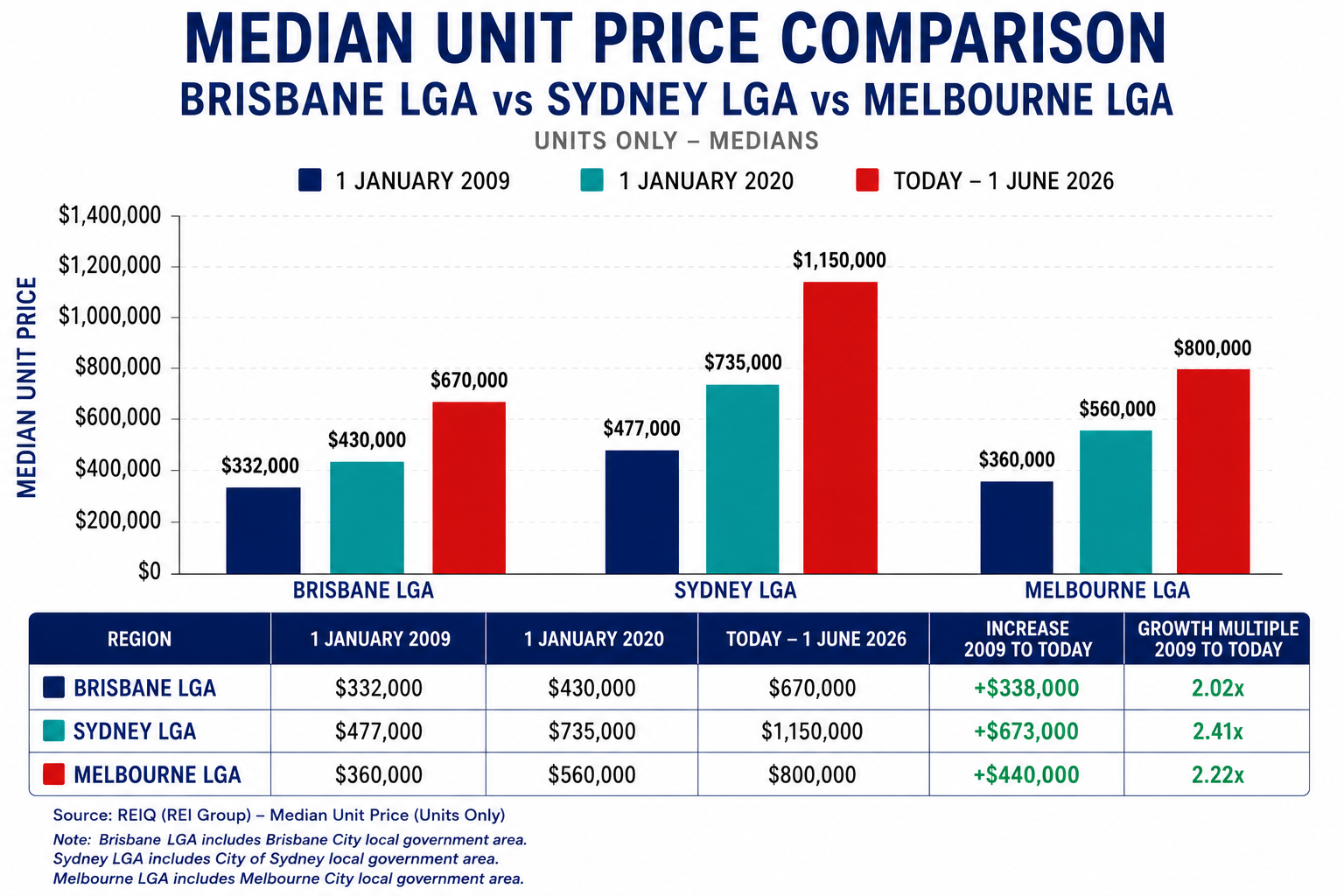

The below image shows that units in Sydney and Melbourne also grew strongly, with the Sydney median unit price of $1,150,000 now very close to the Brisbane median house price $1,220,000.

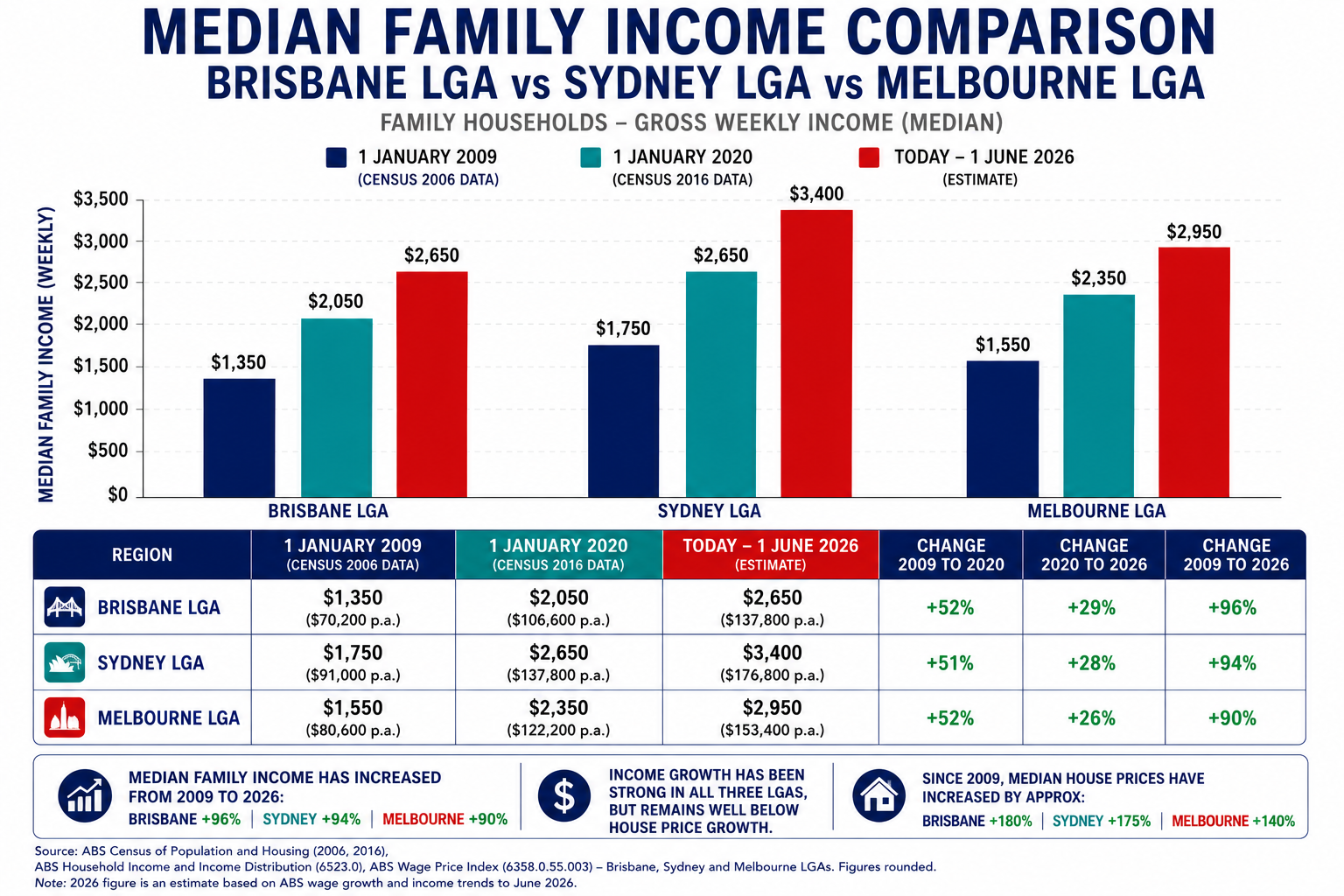

So, if units in all cities have more than doubled, what about median family income to allow for the purchases?

It’s clear that median income growth was surpassed by capital growth for houses and units.

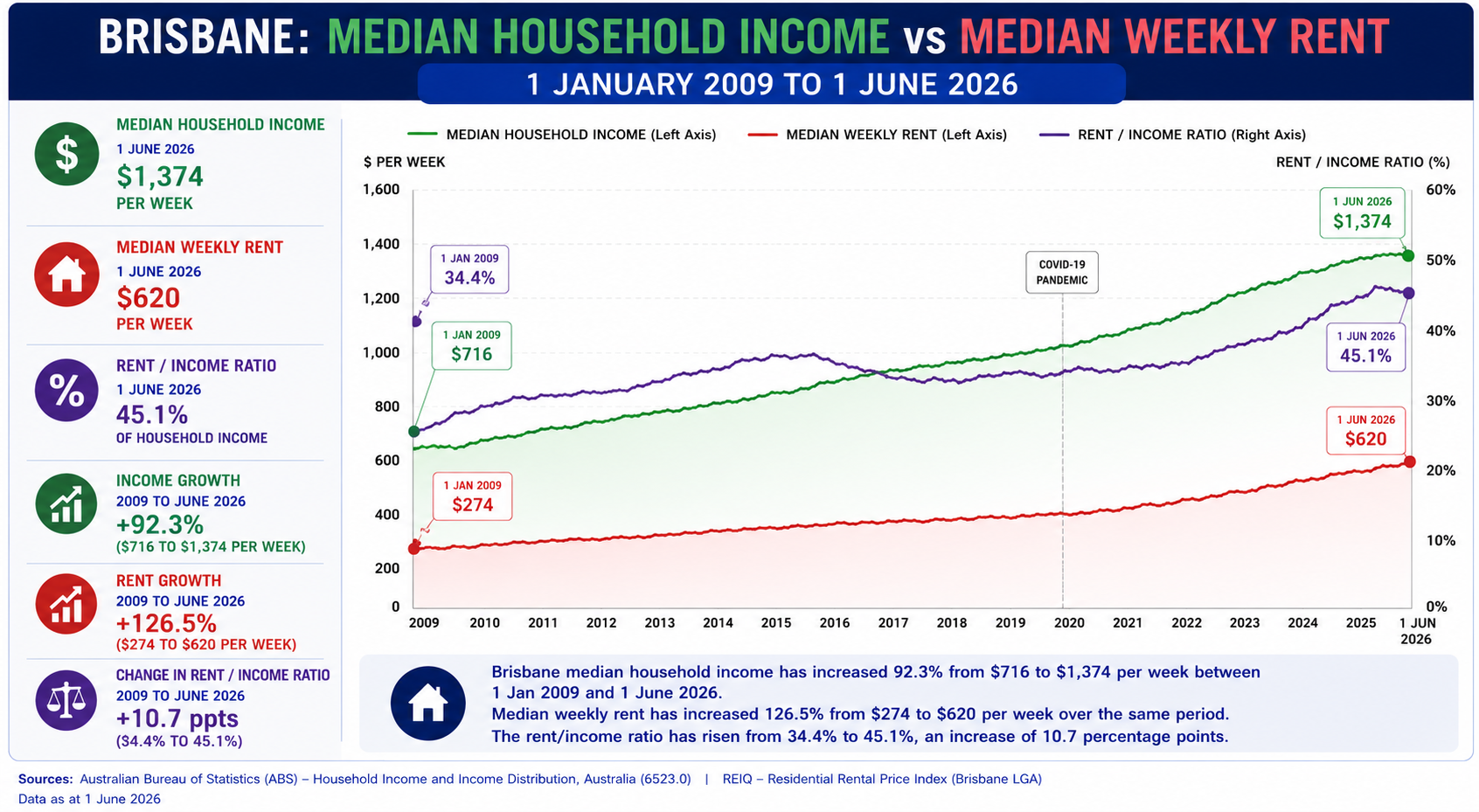

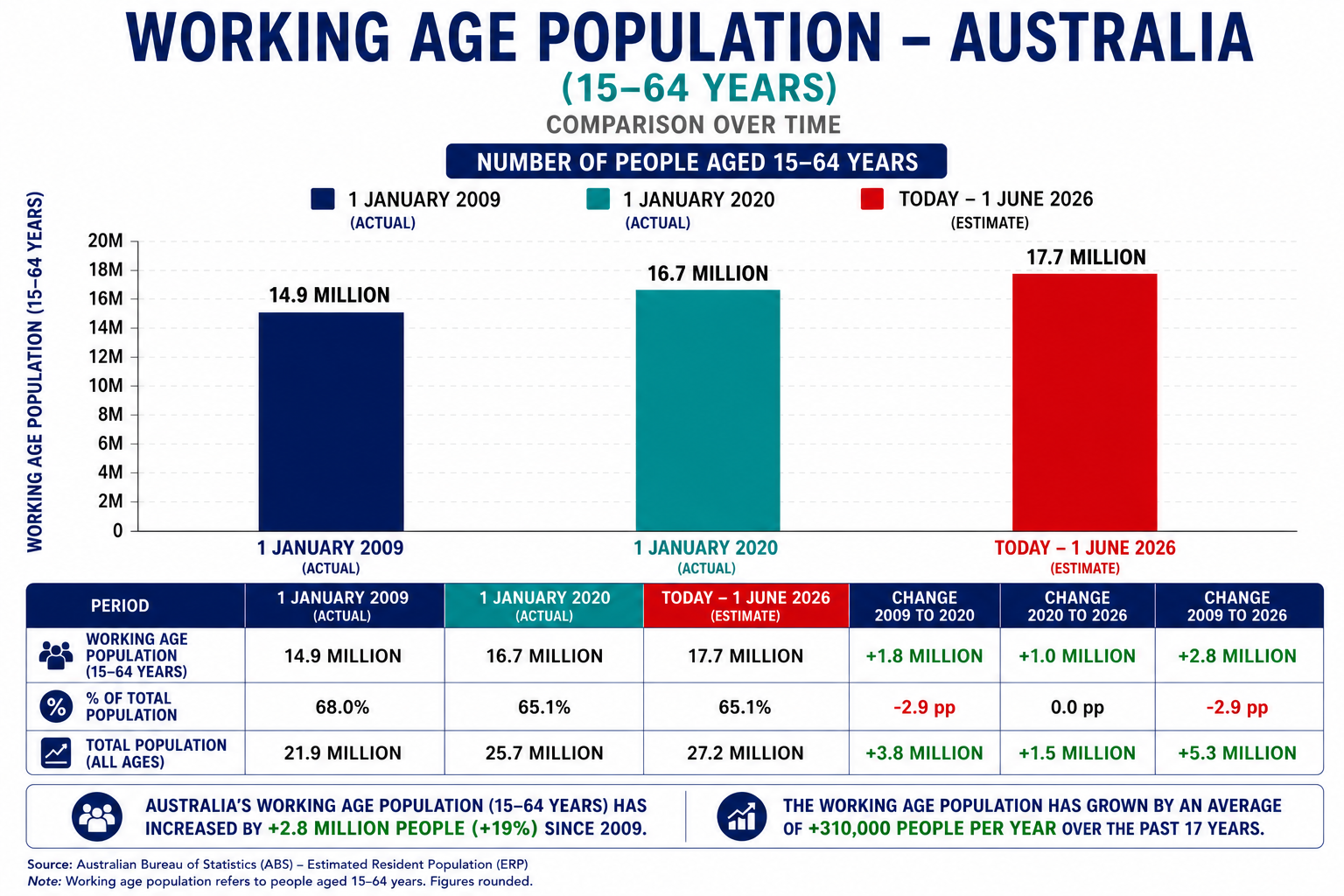

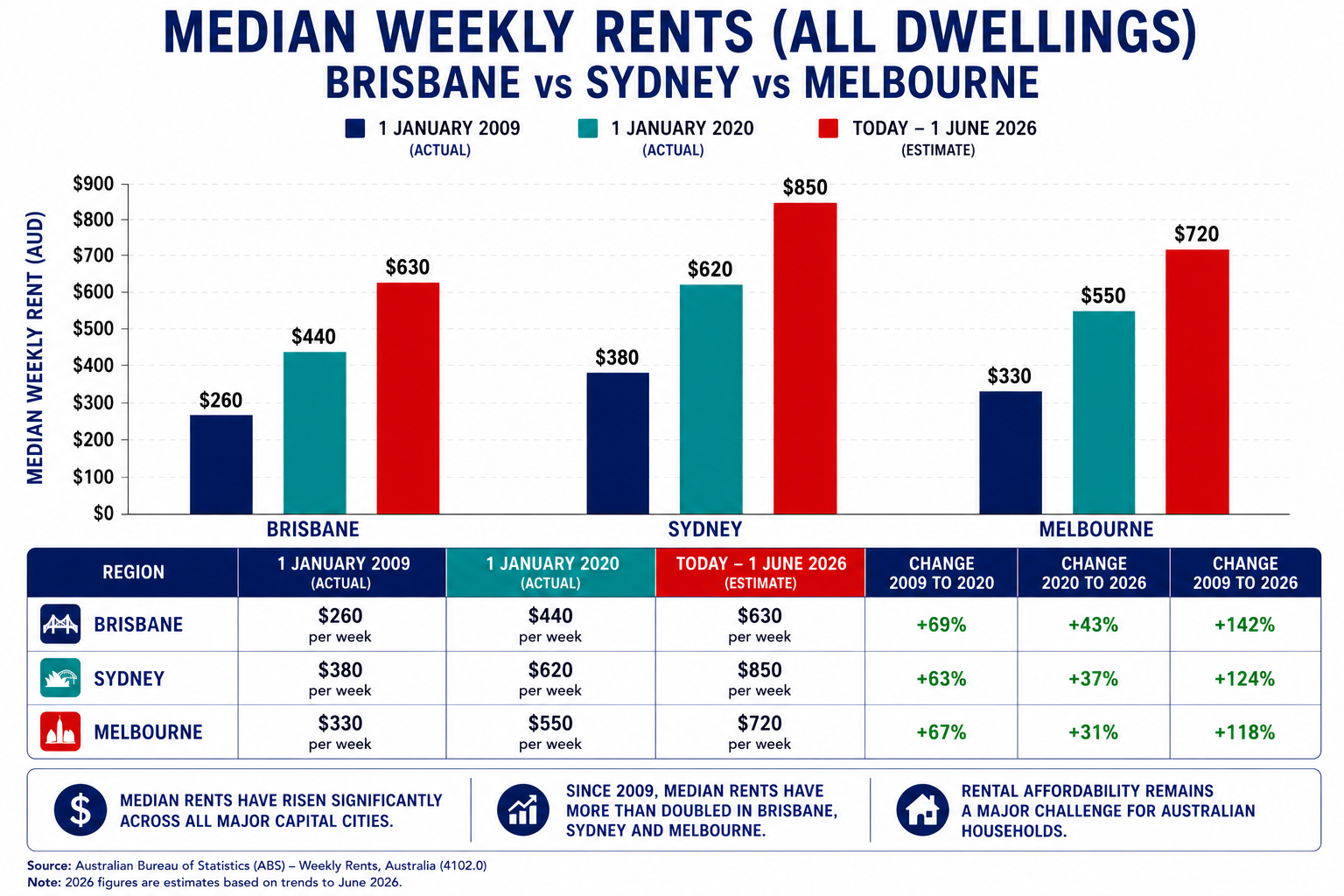

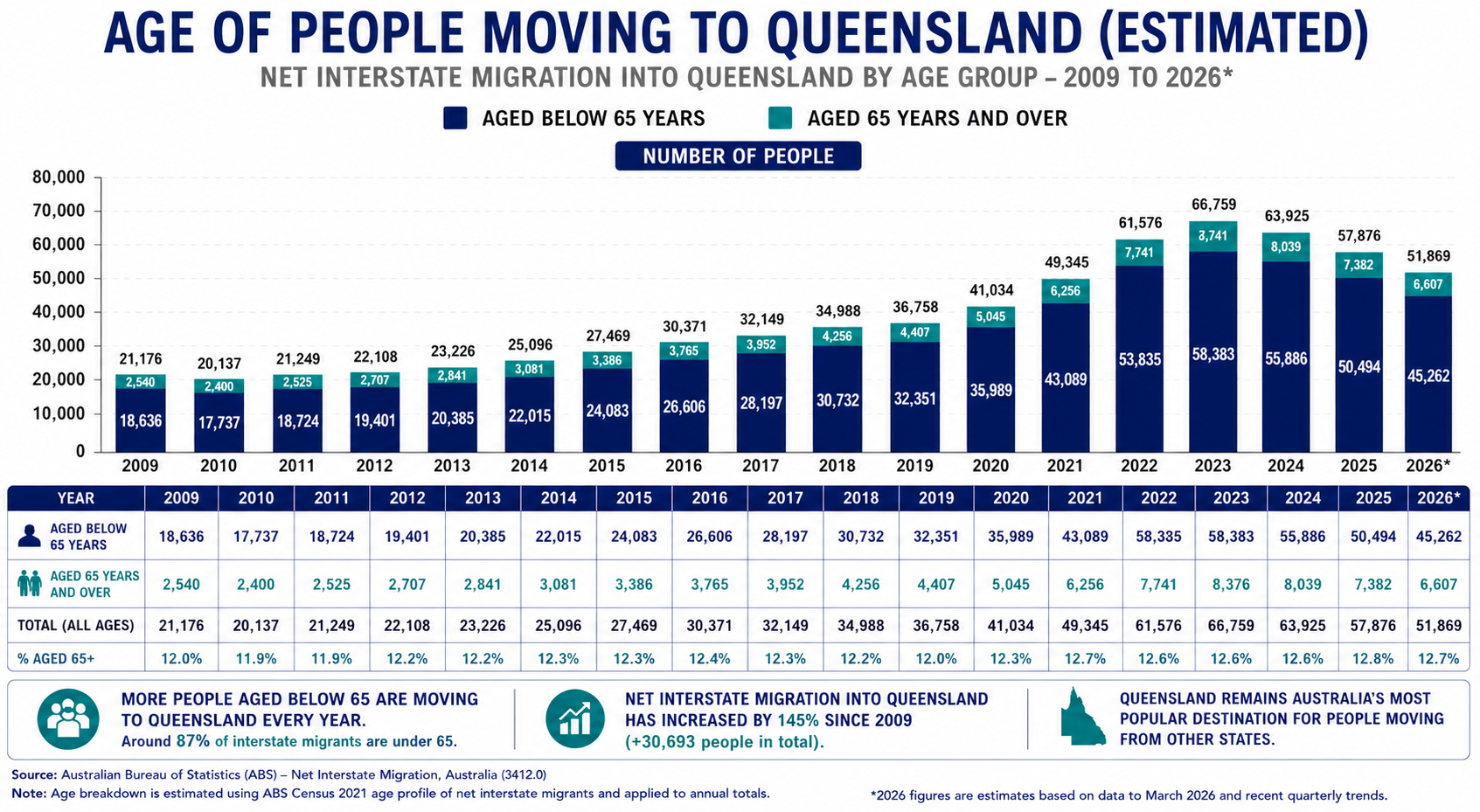

Rents also grew as a percentage of median family income from 34.4% to 45.1% so it’s become harder for renters and better for investors. Now, let’s look at some demographics. Our working age population grew by 2.8m people over the period.

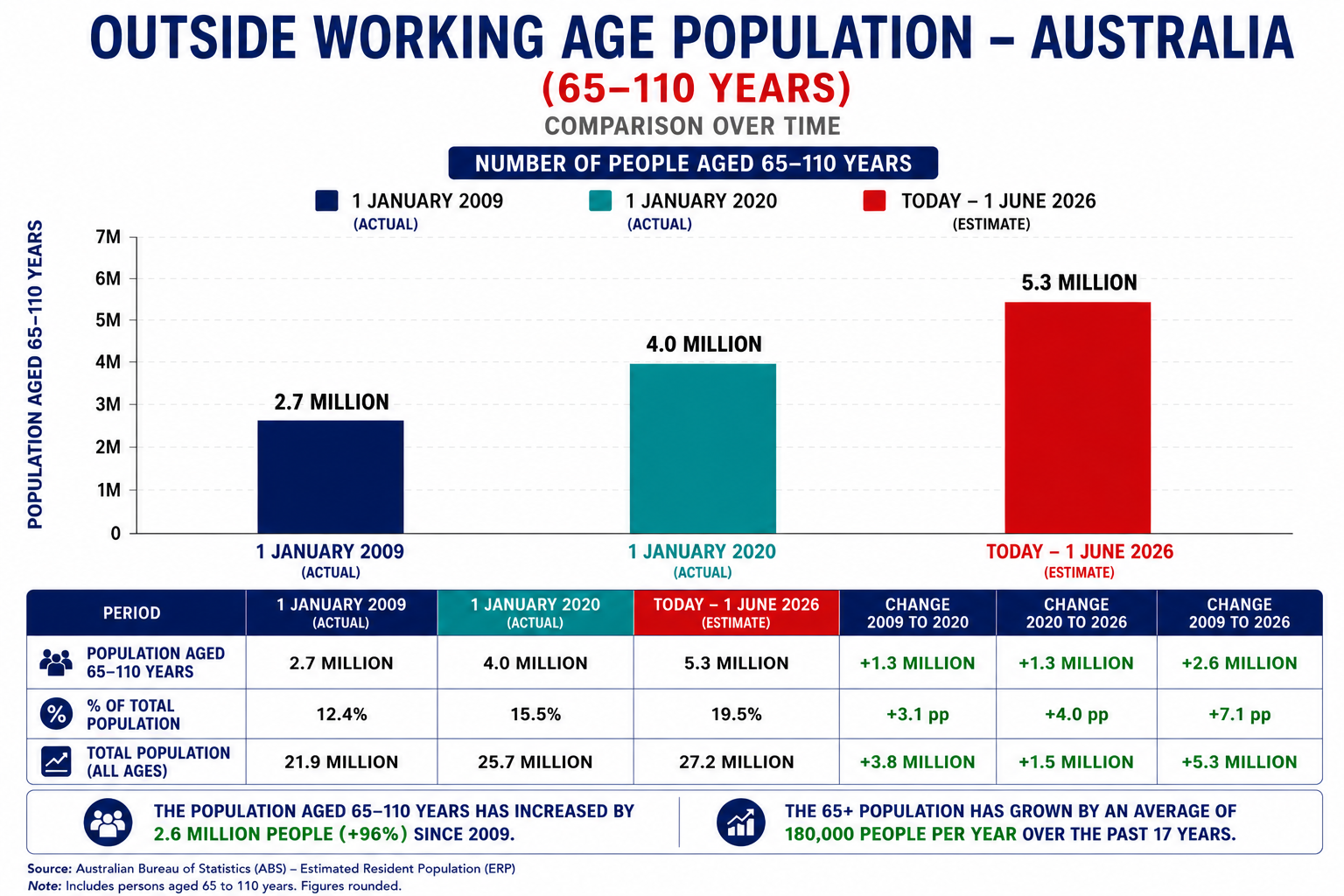

The population over 65 grew by a very similar amount, 2.6 million.

Without immigration, we would have likely had higher growth in retirees than workers. In other words, we would have had higher growth in the number of people who have access to capital versus those still working to generate income and build capital assets. You can start to better understand the Government’s policies in looking to extract more tax revenue from capital gains. We can all also understand that their other option is to cut back on spending on the other side of the equation. With a Labour government, that idea certainly goes against their regular school of thought. So, what about that hot topic of immigration?

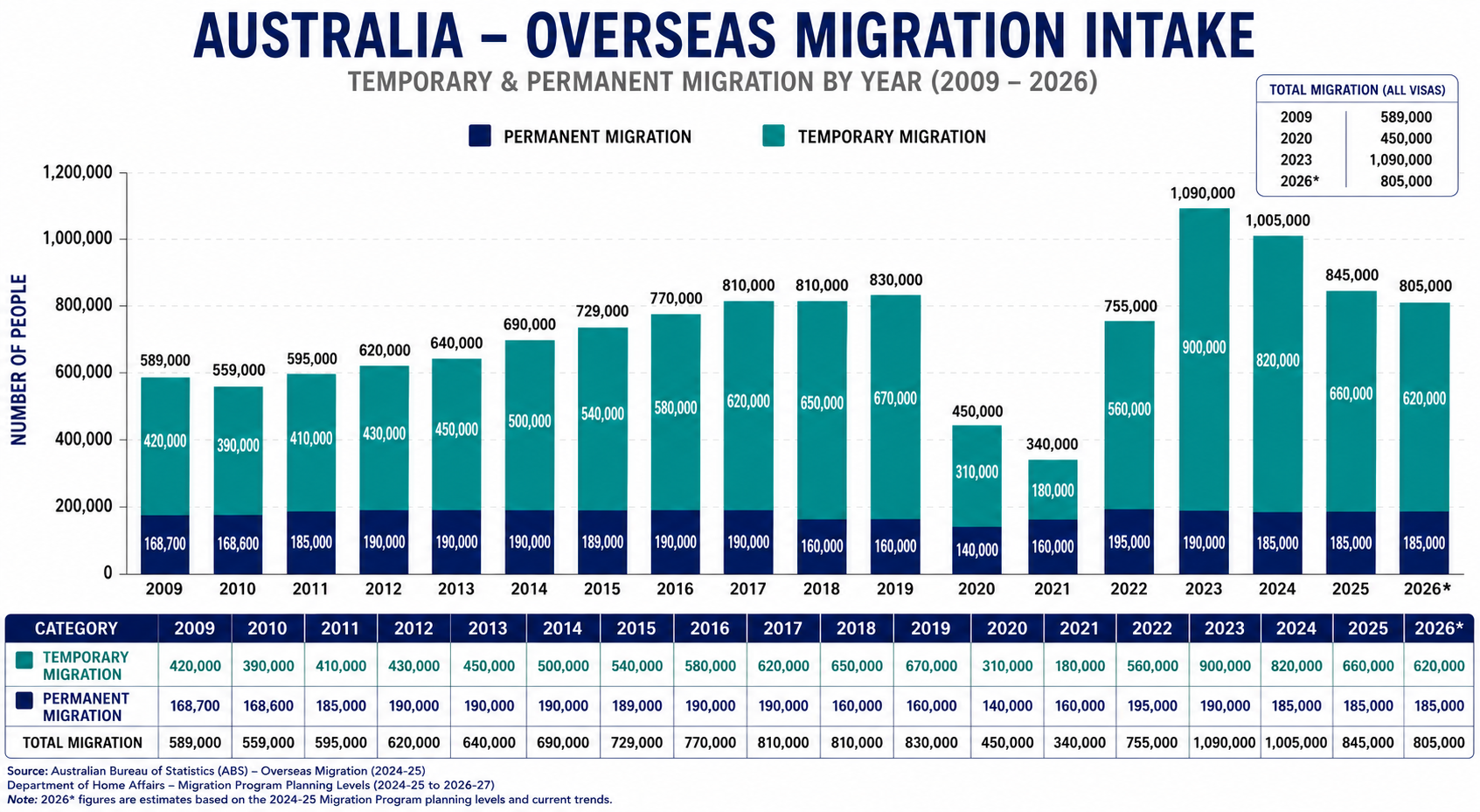

We had total immigration of 4,639,000 from 2014-2019 and 4,485,000 from 2020-2025 when most of the price growth occurred. So, funnily enough, it doesn’t seem like it may have been a sudden population spike that caused the problem, although that’s the narrative we’re certainly used to hearing. The population grew at the same time that we all became more obsessed with owning property. Prices rose as many of us felt the very real fear of missing out.

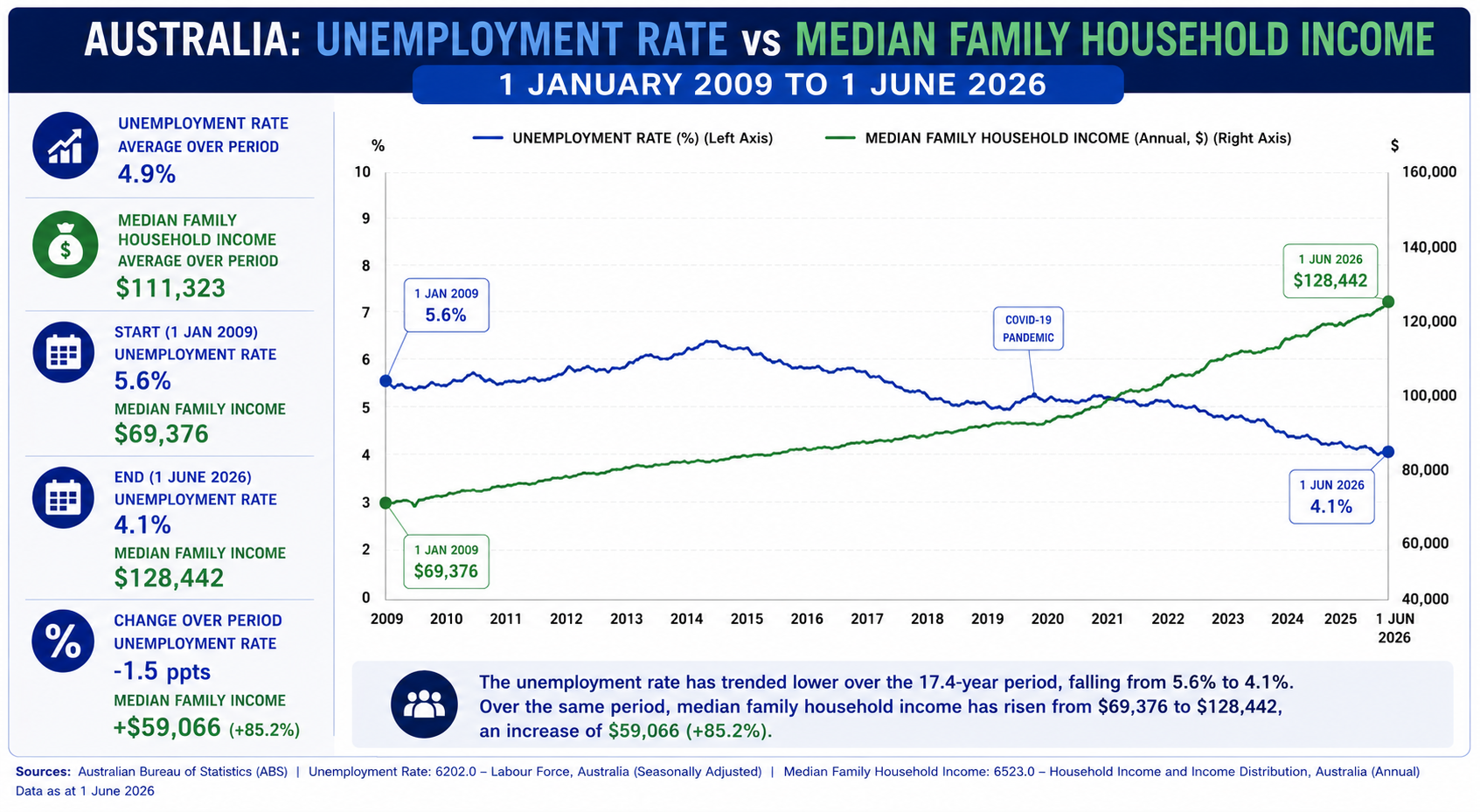

At the same time, median family household income Australia grew by 85% while unemployment dropped from 5.6% to 4.1%. We had more people in Australia and they were more employed. Rents also grew by between 118% - 142% over the period against income growth of 85%.

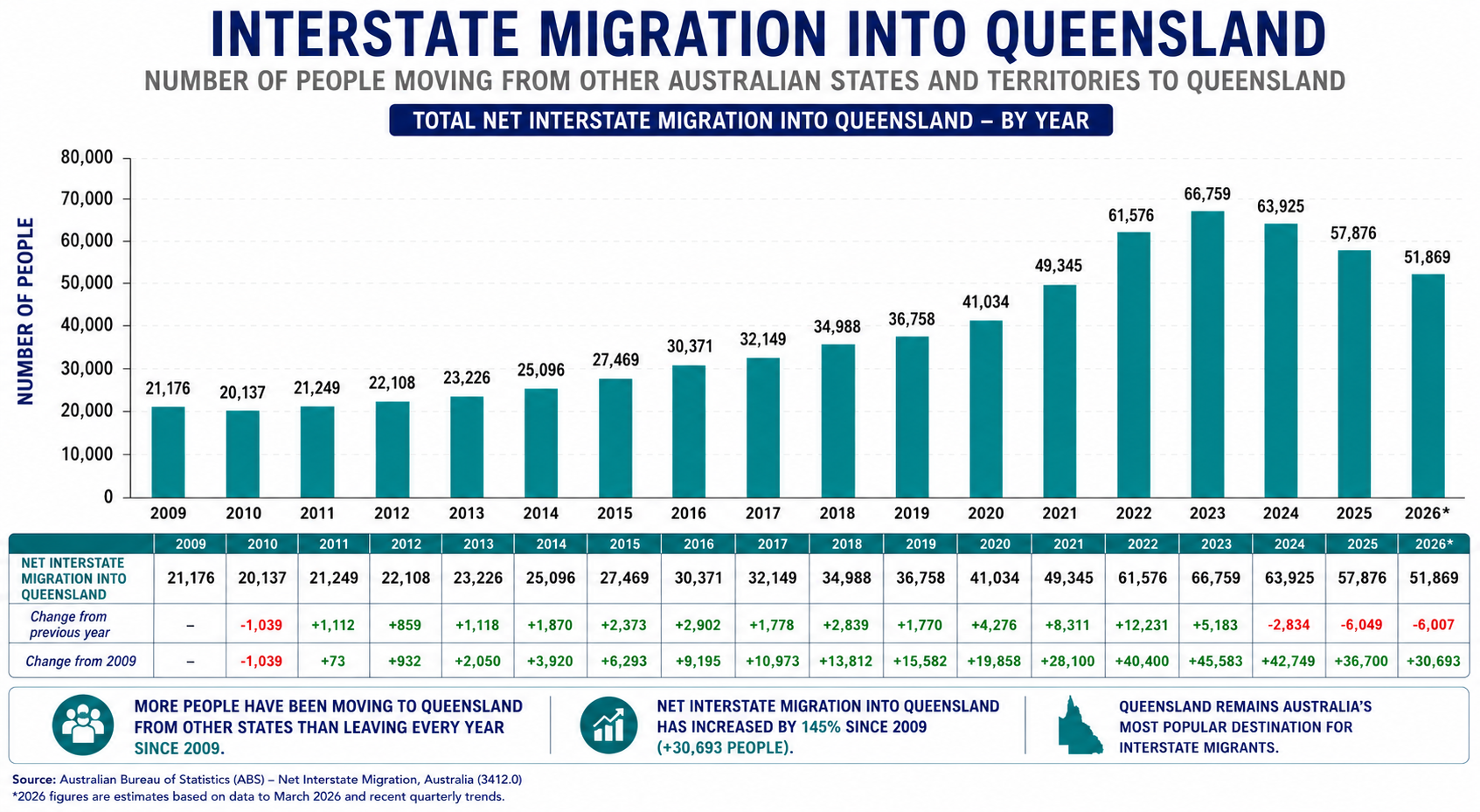

Brisbane’s rents grew the fastest off the lowest base. So, what about interstate migration?

Between 2014 to 2019, we had 186,831 people decide to become Queenslanders. From 2020 - 2025, there was 340,515. We were the most popular state for Aussie migrants and we took in 82.26% more interstate migrants between 2020 - 2025 than 2014 to 2019. There’s a popular story that people from Sydney and Melbourne move up here with wads of cash to buy property but it’s hard to know the full truth. What is clear is that the migrants are working age, as below.

The good news is that we’re not like Florida in the USA. People don’t move here to retire, they predominantly move here to work and raise families. So, we’ve had interstate migration and overseas migration. Have we also seen a growth in housing supply?

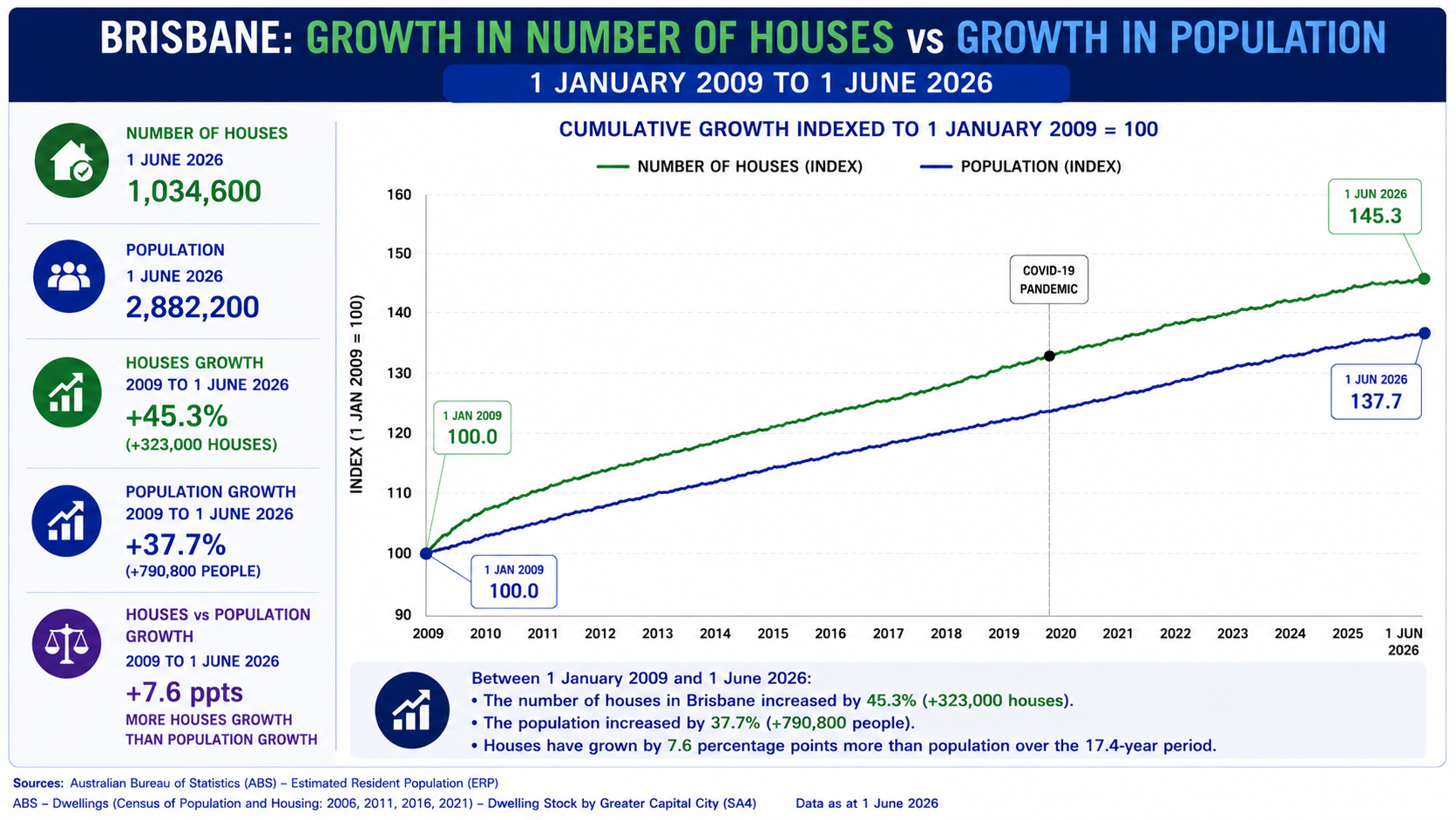

According to the data above, we saw housing supply in Brisbane grow faster than population. In June 2026, there was 1 house to every 2.79 people.

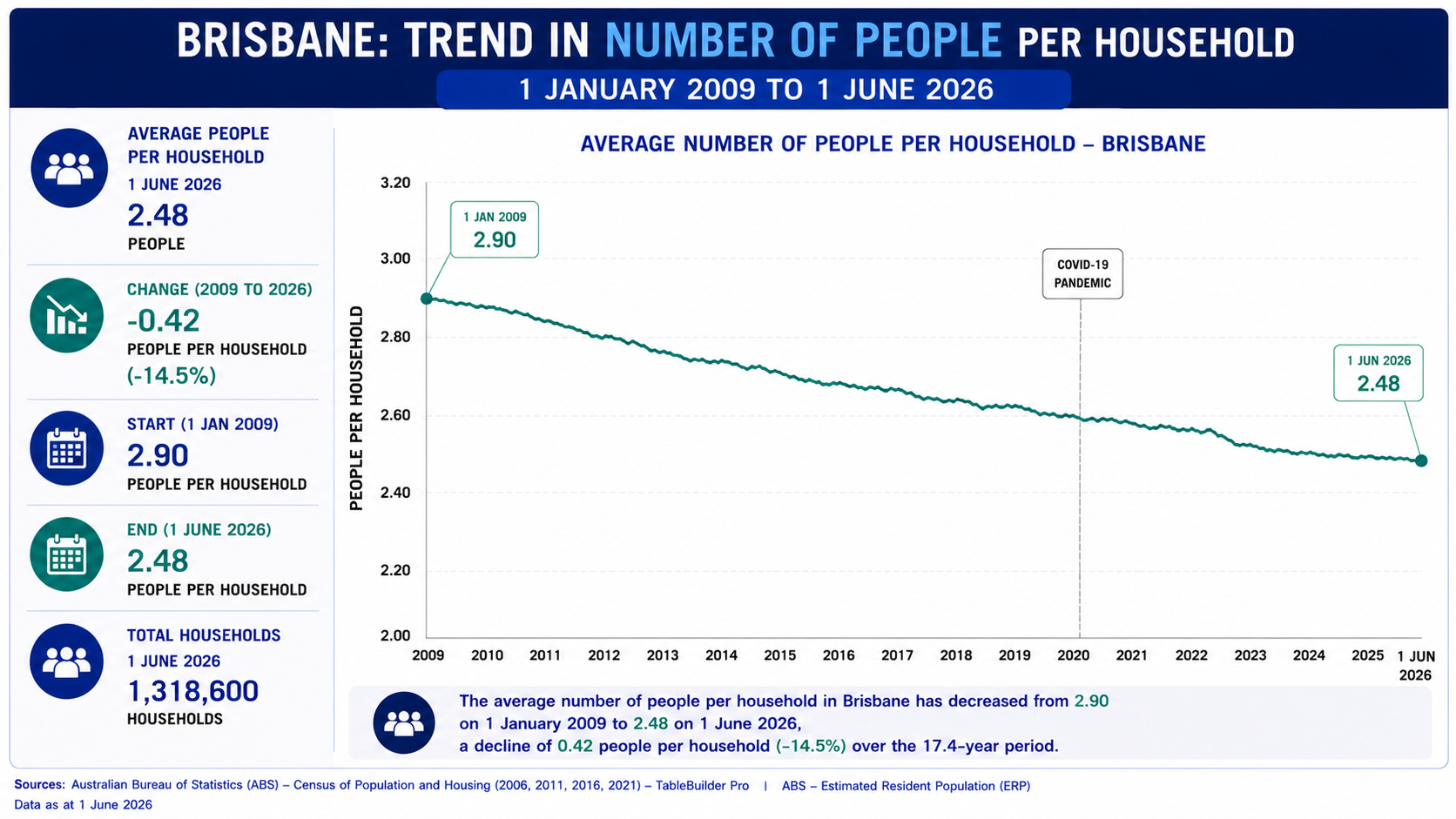

Over the period, we also saw the number of people per household fall from 2.9 in 2009 to 2.48 in 2026, so we had more dwellings with less people in each of them.

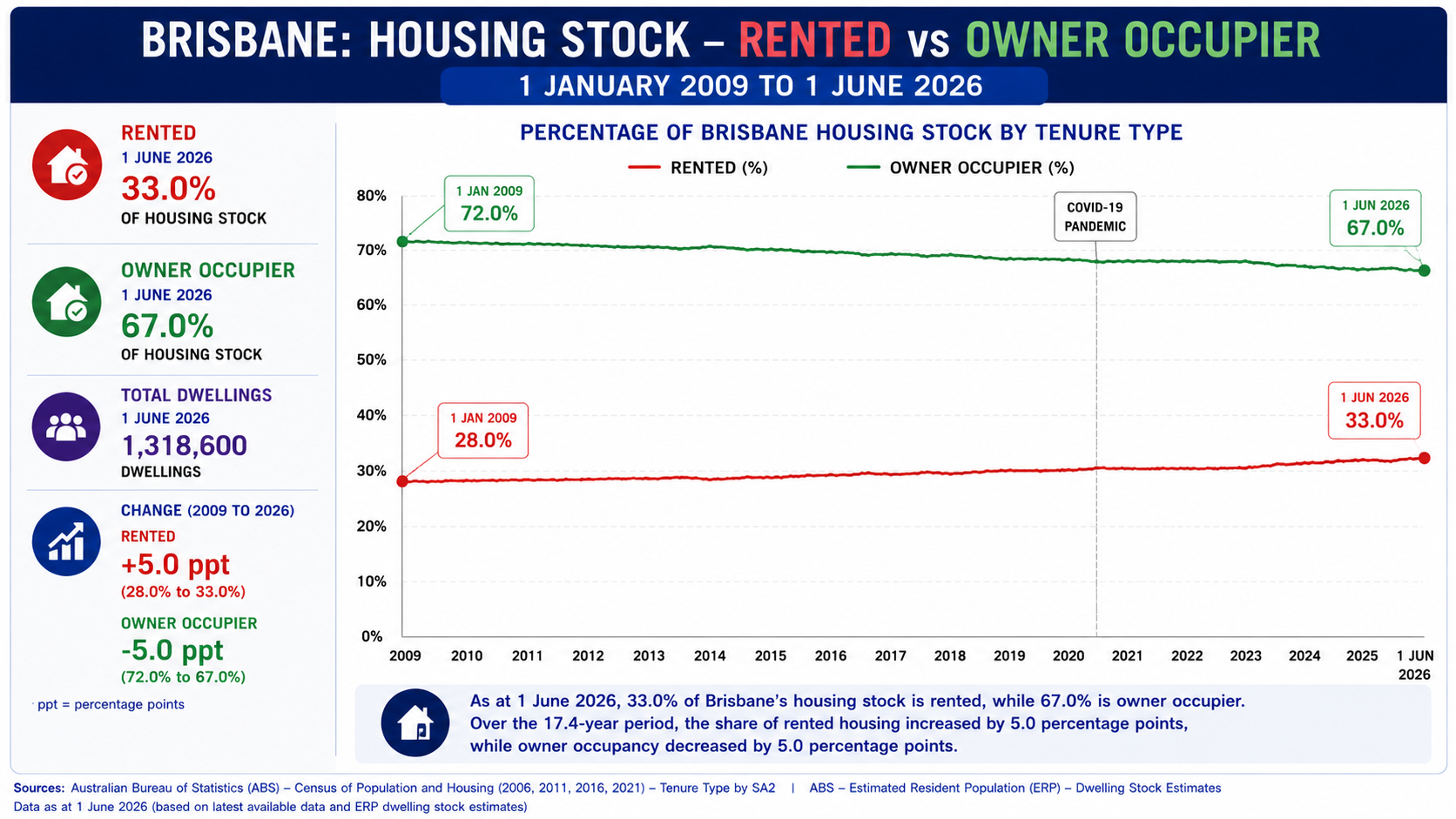

We also saw an increase in the percentage of rental properties from 28% in 2009 to 33% in 2026. So, rents increased while the proportion of investor owned properties also increased.

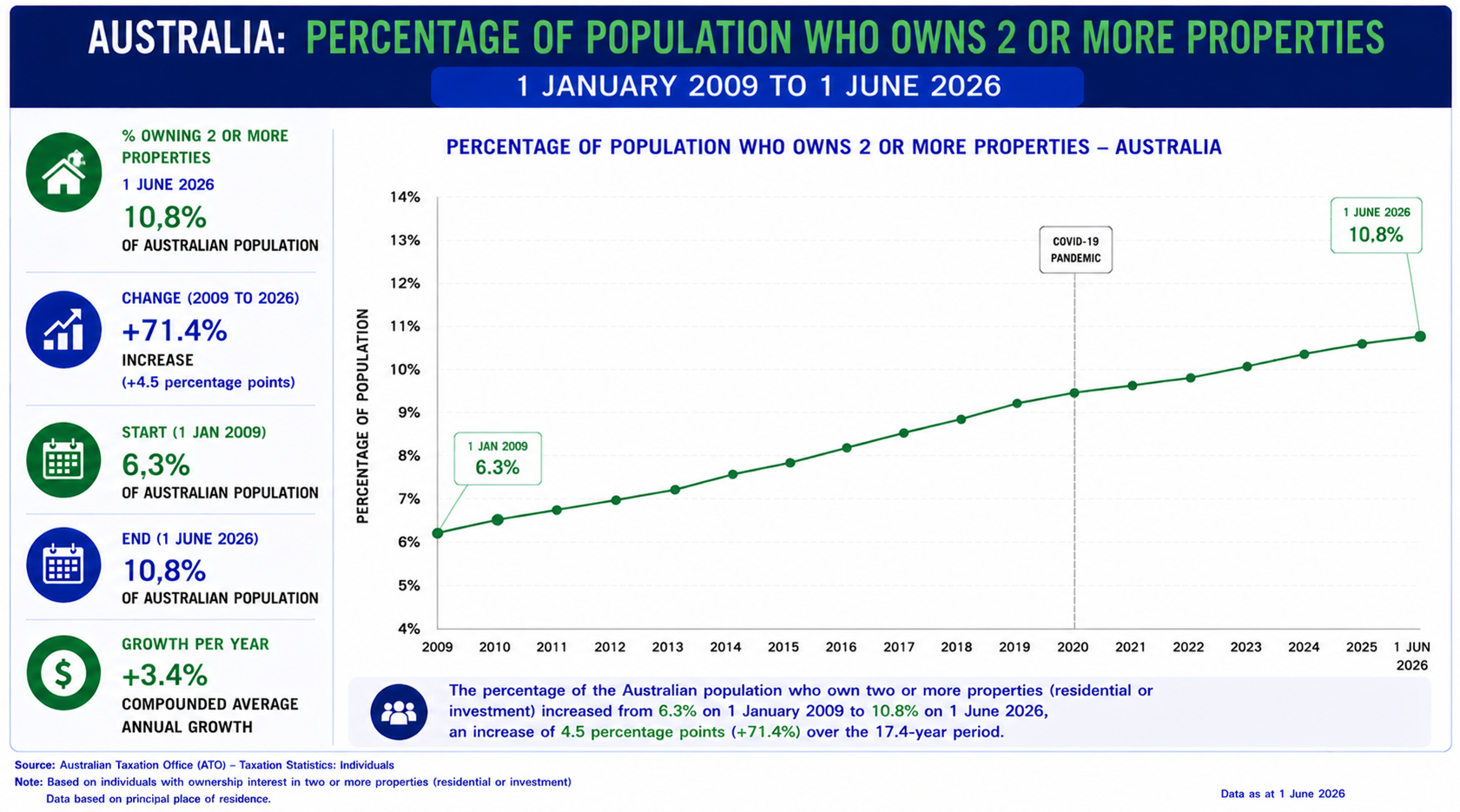

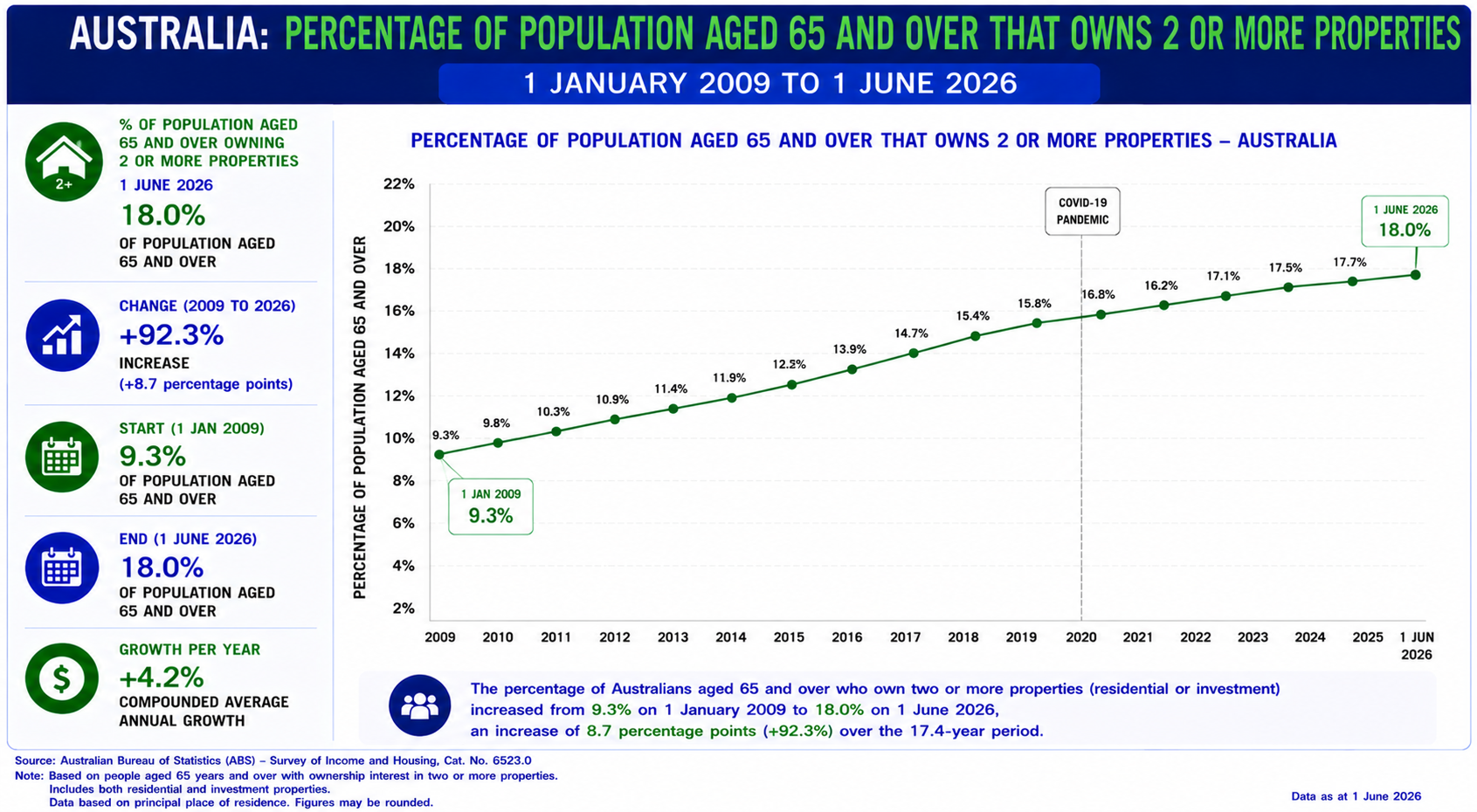

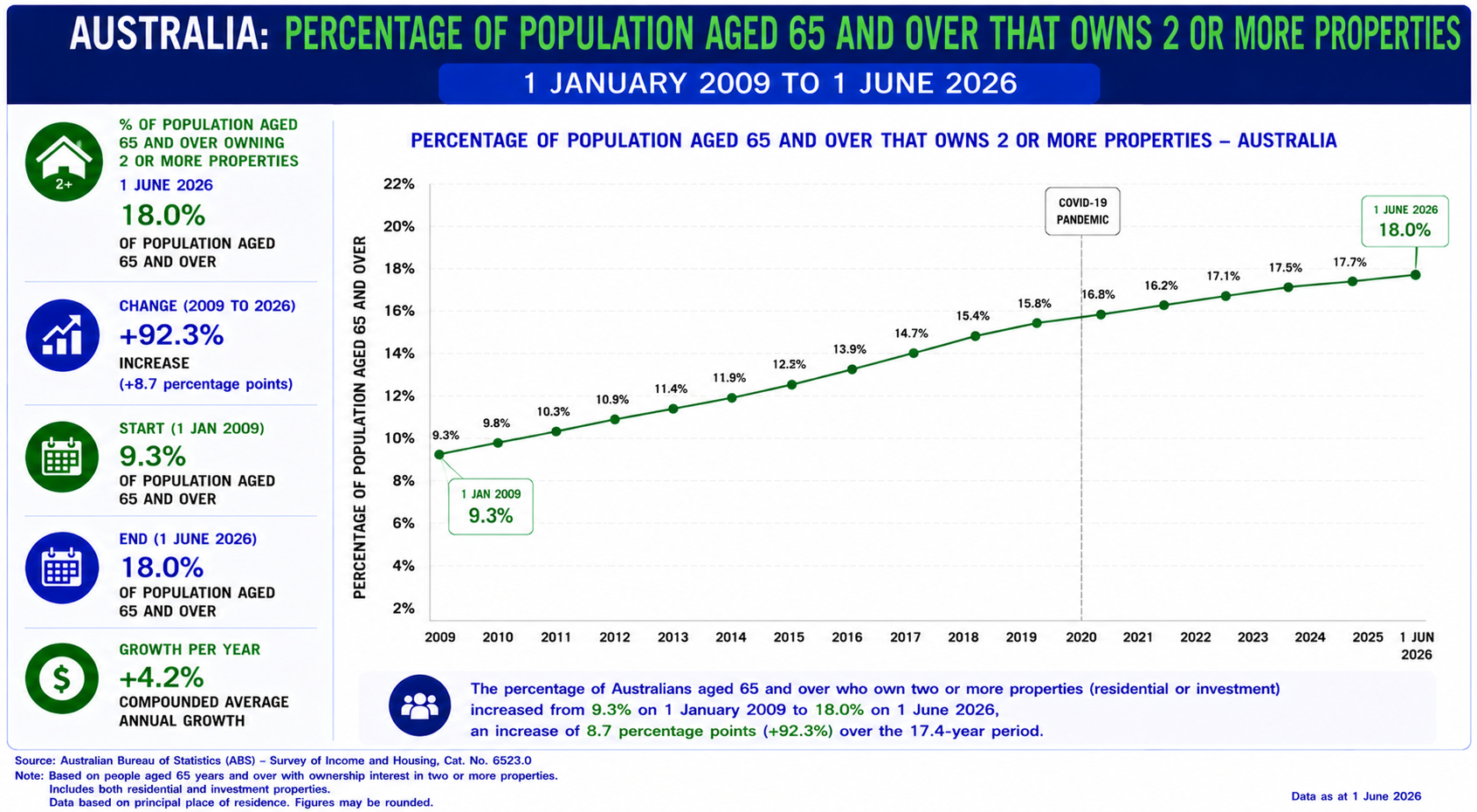

Across Australia, the percentage of population that owns 2 or more properties increased from 6.3% to 10.8%. There was also a significant increase in rental properties for retirees, as below.

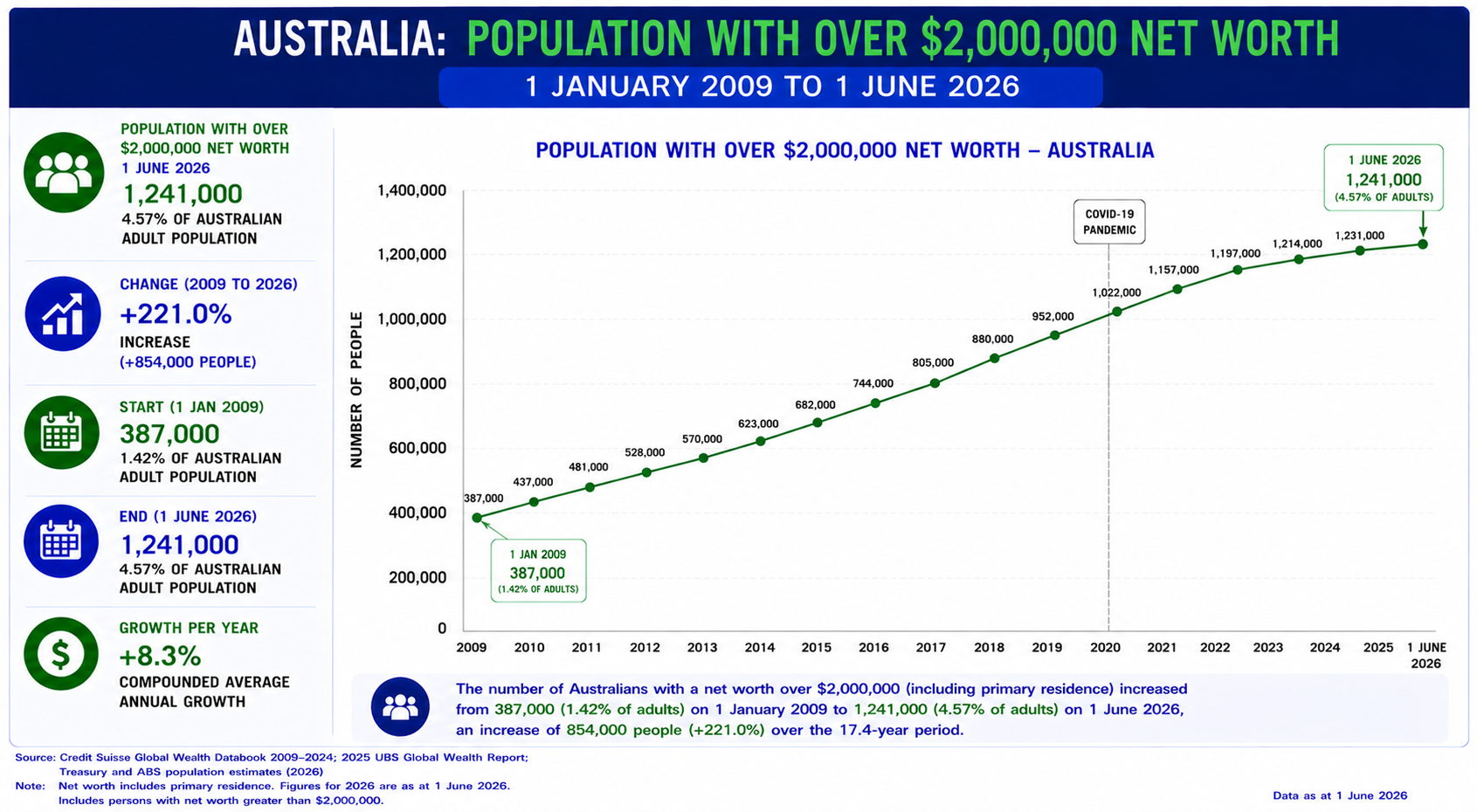

There was also a large shift in Australia’s population with over $2m net worth. I expect much of this also came from property. If most of it was held in their PPR, this also meant that they could likely sell with minimum taxation. If most properties sell and settle within 3 months, this is fairly ready access to capital, tax free capital.

In 2009, there were 387,000 Aussie with net worth higher than $2m. That’s now more than tripled to 1,241,000. So, is it all capital growth or have some incomes also risen?

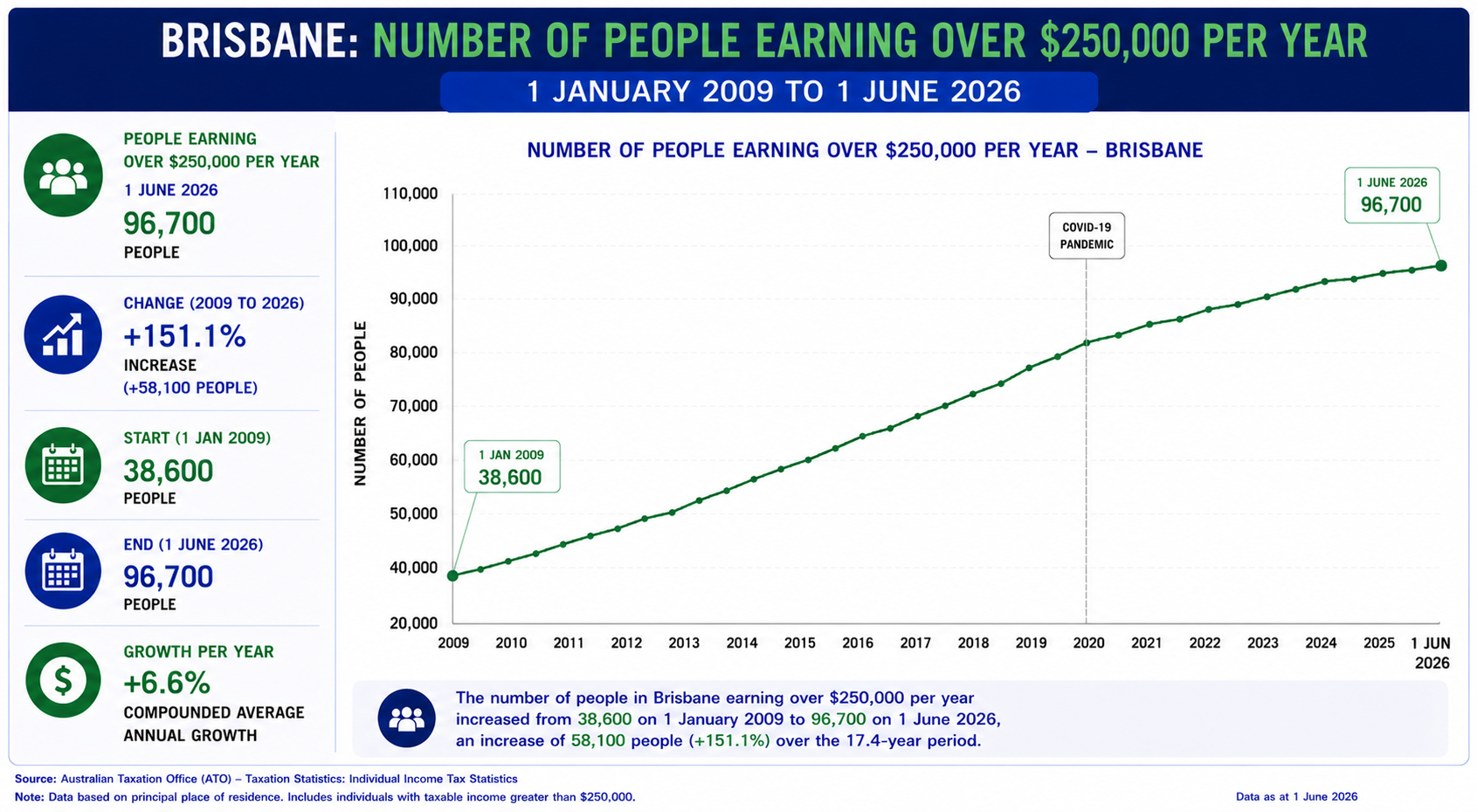

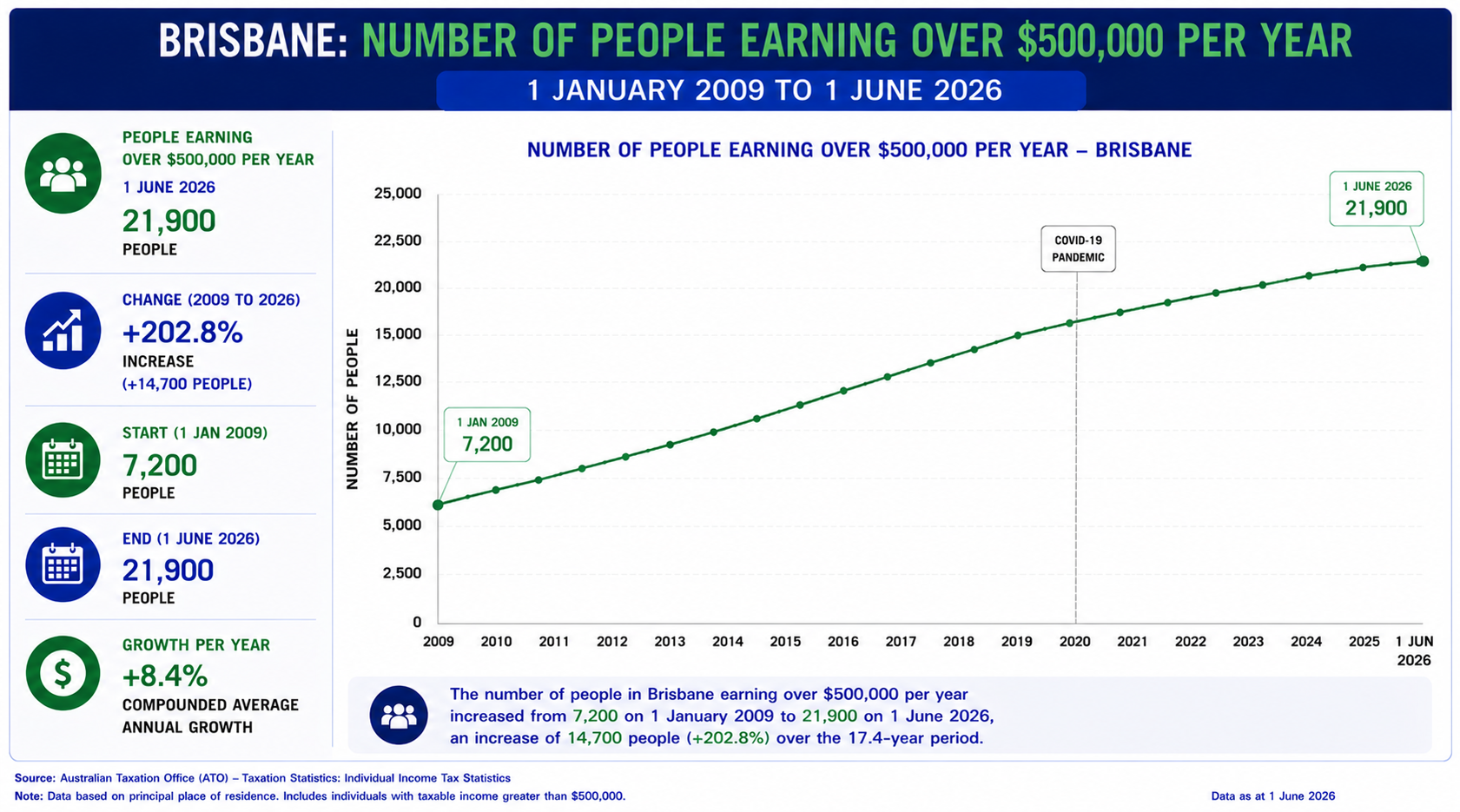

There are now 58,100 more people in Brisbane than there was in 2009 that make $250,000 or more. The number of people making $500,000 or more has also tripled since 2009 to 21,900 people, as below.

Now, as people who’ve worked in property, we’re used to seeing people spend as much as they possibly can to buy a beautiful house for their family in the best possible suburb. There are other people who already own an awesome house and suddenly have access to more capital. These are the people who decide to put their excess capital into stocks or property and will be impacted by these new capital gains taxes. For those of us under 50, much of our income goes towards servicing the debt on our PPR or looking to upgrade into a bigger house or a better suburb, or both.

I made the decision to switch into selling property rather than stocks because I wanted to deal with more regular people. I wanted to sell more to my peers rather than just retirees. Many of us have started making more money, plenty of young people are now better paid and we’ve all now caught the property bug since Covid. We’re starting to see some scary headlines in the media but I can tell you that property is still far easier to sell to a wider audience than stocks or bonds.

I can’t be sure whether property will beat stocks over the next decade but real estate agents often sell a more tax effective asset with higher leverage than stockbrokers. That means you get a larger commission of a bigger asset that also doubles as a place to live or receive rents.

Geoff Wilson from Wilson Asset Management, the funds management arm of the stockbroking firm where I first worked in 2008, would be happy to see properties get taxed harder than stocks as he sees them as “unproductive assets”. That doesn’t change the fact that Aussies love property and we can all easily understand the investment proposition, as can retirees.

I’m no longer an agent, I now coach agents. At one point I may have been your competition, I’m now on your team, if you want. I’ve given you all the data to help you tell a more compelling story about the broader market. The next step is for us to work directly together.

Over the first 4 sessions I’ll help improve the story you tell when you first walk through the door to increase listing conversions, build better relationships with your clients and allow you to be more yourself along the way.

After that, we’ll have 8 sessions to work on whatever you like. I learned from the best in both property and finance here in Brisbane & Toronto, Canada. My focus is now on helping you become the best possible real estate agent while I continue to coach my wife, Dani, in her role as a buyer’s agent here in Brisbane and surrounds.

The First Four Sessions are outlined below and are carried out on a weekly basis during the first month.

The following 6 sessions are guided by you. We'll work through whatever you bring to the table over the following 6 months.

At the end of the 10 sessions, my goal is for you to never have to see me again. You can just get on with achieving your goals.

Session 1 - We walk through the warts and all story of everything that’s happened up til now so that it exists in reality, not just in your own head. Once we have that sorted, we do some personality testing to learn more about you to work on next week.

Session 2 - We do an in depth review of your strengths and weaknesses, as you see them, to see exactly what you bring to the table. We also work through the results of the personality testing so you can learn more about how someone like you usually shows up in the world and the strengths and weaknesses associated with your personality type.

Session 3 - This is where we take stock of all the work we’ve done so far, reassess all the weaknesses and strengths then record a more positive story that you can use to play back to yourself at times when you may be feeling less confident or less accomplished. Effectively, we’re rewriting the story that plays in your head so you can tell a better one in all future encounters.

Session 4 - This is where the rubber hits the road. We’ve worked on the story, we’ve worked on understanding your strengths and weaknesses and now we build a plan of attack to make it happen to help you achieve your goals.

The Sales Training Program is also included in the package based on the extensive training I received here in Brisbane as well as at Keller Williams Real Estate & Investors Group Financial Planning in Toronto, Canada

Feel free to reach out on 0424 682 636 if there’s anything else you need.